The essential banking customer service guide

What financial institutions need to know

How to optimize contact center operations, drive digital adoption and build lasting customer trust

Table of contents

- The high stakes of trust in financial services

- Top challenges facing banking contact centers

- Common mobile banking issues and how to prevent them

- Proven strategies to drive digital banking adoption

- Key trends shaping banking and finance support for 2026

- Best practices for optimizing your contact center

- Scaling effectively with self-serve support

- Turning customer service into a competitive advantage

The banking world is increasingly digital, with 83% of Americans using finance apps for their everyday banking and payments. However, providing the right technology is only half the battle. Good customer service is a critical factor for business success. In fact, one in four customers is thinking of switching financial service providers, primarily for better service.

This comprehensive guide explores the current landscape of banking customer service, common challenges and actionable strategies to optimize your support ecosystem.

The high stakes of trust in financial services

In banking, the stakes for customer service are uniquely high. Customers are trusting your institution with their savings, pensions and sensitive personal information. Consequently, trust is the number one factor for customers choosing a financial services provider.

When customers experience poor support, such as inaccurate information or inconsistent guidance, it creates a perceived risk regarding their financial safety. Instead of formally closing their accounts, frustrated customers often engage in "soft switching," where they gradually transfer their money to a competitor.

Top challenges facing banking contact centers

As institutions attempt to scale their digital offerings, they face several critical hurdles that strain support budgets and impact the customer experience (CX):

- High agent turnover: Contact center agent turnover sits at a staggering 45%, and replacing an employee can cost double their salary. This revolving door leads to longer average handle times (AHT) and inconsistent service quality.

- Fragmented and siloed experiences: Many banks use multichannel support environments where phone, chat and email systems are disconnected. This fragmentation forces customers to repeat themselves, increasing resolution times and customer frustration.

- Legacy infrastructure: Older contact center systems can consume up to 80% of an IT budget in maintenance fees, limiting a bank's ability to invest in modern digital experience improvements.

- Security and fraud risks: Financial organizations experience up to 300 times more cyberattacks than other industries. Balancing fast customer service with rigorous security measures (like multi-factor authentication) is a constant struggle.

Common mobile banking issues and how to prevent them

A seamless mobile app experience is essential for retaining customers. To reduce ticket volume, institutions must proactively address these common mobile banking issues:

- Ignoring key performance indicators (KPIs): To truly improve app support, teams must monitor metrics like first-contact resolution (FCR), churn and average handle time (AHT) to identify where customers are getting stuck in transaction flows.

- Payment and transfer confusion: Ambiguity surrounding transaction statuses frequently drives high support ticket volumes. Implementing clear labels like “completed,” “pending” or “failed” alongside proactive in-app notifications can significantly reduce friction.

- Lack of clear communication: Generic error messages like "something went wrong" leave customers guessing. Setting clear expectations upfront regarding how long processes take can mitigate frustration.

Proven strategies to drive digital banking adoption

High digital adoption creates a win-win scenario by drastically lowering business costs (average mobile transactions cost just 10 cents compared to over $4 for in-person transactions) and reducing case burdens on live agents.

To overcome common roadblocks to digital adoption in banking, focus on:

- Prioritizing accessibility: With one in four Americans having a disability, digital banking must offer high-contrast color schemes, screen reader compatibility and accessible fonts. Additionally, allowing users to customize language settings reduces transaction stress.

- Leveraging interactive tutorials: Almost two-thirds of people are visual learners, making static FAQ articles ineffective. Interactive tutorials increase engagement by over 50% and empower users to learn new digital features at their own pace.

- Boosting digital literacy: Older generations may resist digital tools due to long-standing habits and low digital literacy. Offering in-branch workshops and accessible learning resources can gently introduce them to digital platforms

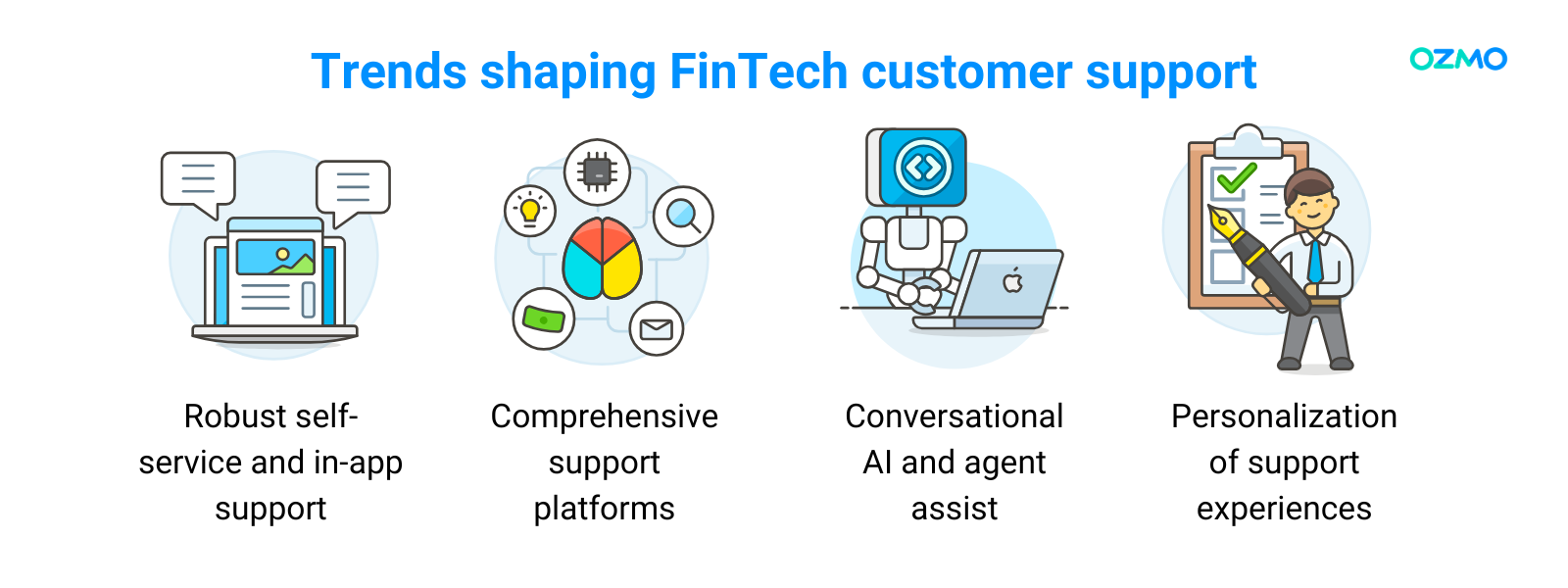

Key trends shaping banking and finance support for 2026

To stay competitive and reduce churn, modern institutions must invest in scalable finance app customer support strategies:

1. Robust self-service and in-app support

Self-service empowers customers to handle high-frequency tasks (e.g., balance checks, card freezing, password resets) independently, which lowers overall call volume and reserves live agents for complex cases. This is particularly critical for capturing the Gen Z market; Gen Z customers demand mobile-first experiences and will hang up if left on hold for less than a minute.

2. Comprehensive customer support platforms

Unlike siloed multichannel setups, where customers frequently receive conflicting answers depending on the channel they use, a true omnichannel approach unifies all service information into a single platform. This creates a single source of truth, ensuring that whether a customer reaches out via the mobile app, SMS, chat or phone, they receive the exact same, accurate answers. By combining this unified knowledge base with retained interaction context across all touchpoints, agents have full visibility into the customer's history. This eliminates the need for customers to repeat themselves, streamlines resolutions and ultimately boosts first-contact resolution (FCR) and Net Promoter Scores (NPS).

3. AI integration: Conversational AI and agent assist

Currently, 68% of financial services customers use AI for banking. Here are two options for incorporating AI in banking customer service.

- Conversational AI: Moving beyond traditional keyword-based chatbots, conversational AI uses large language models (LLMs) to understand the context of user requests and provide instant, accurate troubleshooting.

- AI agent assist: Instead of replacing humans, successful institutions use AI to augment agent performance. Agent-assist tools analyze customer data in real-time to provide live agents with the most accurate diagnosis and resolution steps, drastically improving productivity.

4. Deep personalization

Over three-fourths of customers are frustrated by a lack of personalized interactions. Providing customized support — such as suggesting relevant products based on goals, offering support in preferred languages or giving credit score tips — differentiates a brand. Institutions that successfully implement personalized experiences can see revenue increases of up to 40%.

Looking to transform your digital banking support?

Discover real-world app support

Modernize legacy systems with Ozmo’s robust banking support software.

Best practices for optimizing your contact center

While digital channels are growing, the live contact center remains the backbone of handling complex financial disputes and emotionally charged customer issues. To optimize your financial services contact center operations and prevent the high costs of agent turnover, focus on the following strategies:

- Revamp agent onboarding: Customer service agents with a poor onboarding experience are twice as likely to seek a new job, whereas a strong onboarding program can reduce turnover by more than 80%. To build a resilient workforce, set clear goals for new hires, maintain up-to-date training materials, provide actionable feedback and introduce mentorship programs.

- Deploy agent assist AI: Optimizing operations doesn't mean replacing humans with robots; it means helping agents work smarter. Agent-assist tools operate in the background of live calls, analyzing the customer's interaction history to instantly provide the agent with the most likely diagnosis and resolution steps. This saves agents from hunting across multiple systems for answers, drastically reducing average handle time (AHT).

- Unify the knowledge base (omnichannel): In disconnected multichannel environments, customers frequently receive conflicting answers depending on whether they engage via the app, phone or chat. Additionally, legacy systems make it difficult to consistently update help content across platforms when products or services change. By adopting a true omnichannel strategy, all knowledge and service information lives in a single, unified platform. This creates a single source of truth, ensuring that whether a customer uses in-app tools, sends an SMS or calls a live agent, they receive the exact same, consistently up-to-date answers.

Scaling effectively with self-serve support

Did you know that eight out of 10 customers try to resolve tech support issues independently before reaching out to your contact center? Customer self-service tools such as interactive tutorials are no longer a nice-to-have but a must-have for a successful customer service strategy.

However, most companies aren’t delivering the quality customer self-service their customers expect. This can be detrimental to the success of their business since 96% of customers leave after just one bad service experience.

Digital banking self-service transforms high-frequency, routine inquiries into automated, digital resolutions. When customers can independently perform tasks like viewing balances, depositing checks or freezing a lost credit card, it drastically reduces contact center call volume.

Beyond simply deflecting tickets, a robust self-serve strategy is vital for customer retention, which directly impacts the bottom line — especially since acquiring a new customer can cost up to seven times more than retaining an existing one.

Not all self-service platforms are created equal. When evaluating automated support tools for your financial institution, prioritize the following criteria:

- Compliance and security: Ensure the tool adheres to strict industry regulations and data privacy laws.

- Ease of Integration: The solution must integrate smoothly with your current tech stack and mobile applications to prevent siloed data.

- Data-driven insights: Look for platforms that offer deep visibility into customer behavior, allowing you to track where users succeed or get stuck in self-service paths.

- Scalability and timeline: Assess the projected timeline for implementation and ensure the platform can grow dynamically alongside your business and ticket volume.

Turning customer service into a competitive advantage

As mobile and digital banking adoption continues to skyrocket, delivering high-quality customer support is no longer just a nice-to-have; it's a mandatory requirement for financial institutions. Because financial providers handle highly sensitive personal data and money, providing a reliable, frictionless customer experience is paramount to maintaining the brand trust necessary for business success.

By moving away from siloed legacy systems and embracing scalable strategies, such as AI augmentation, true omnichannel platforms and robust self-service options, organizations can effectively meet customers where they are while managing growing support demands without adding unnecessary costs. Ultimately, modern banking customer service is no longer just a traditional cost center; it is a critical tool for building long-term loyalty, reducing customer churn and differentiating your brand from the competition.

If you're ready to future-proof your support ecosystem, explore how Ozmo's banking and finance support solutions can help you streamline contact center operations and deliver exceptional customer experiences.